Why fiscal consolidations (spending cuts or tax will increase) do not scale back debt to GDP ratios, and why politicians proceed to tighten on the fla

[ad_1]

The declare typically made

for fiscal consolidations (cuts in public spending or will increase in

taxes) is that they’re required to cut back the ratio of public sector

debt to GDP. However whereas fiscal consolidations are prone to scale back

public sector debt, they’re additionally prone to scale back GDP, so the influence

on the debt to GDP ratio is unclear. Analysis simply

revealed by the IMF means that, primarily based on previous

proof, the common impact of fiscal consolidations on the debt to

GDP ratio is negligible (i.e. just about zero).

Wanting on the research

in additional element, the outcomes are even worse for proponents of

austerity. By austerity I don’t imply fiscal consolidation within the

type of spending cuts, however any fiscal consolidation undertaken when

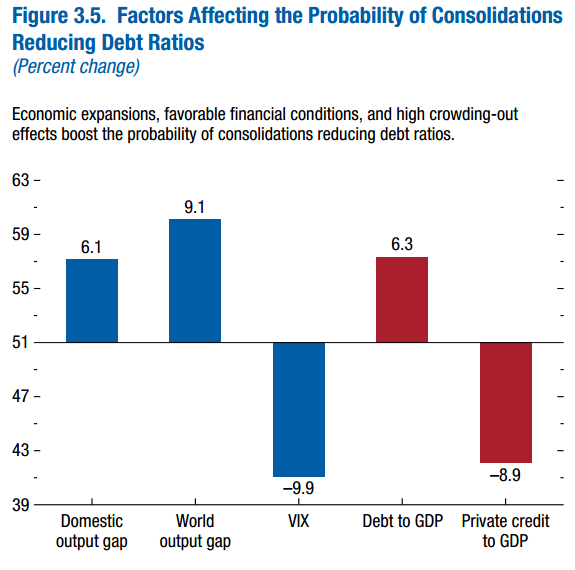

output is beneath pattern. Here’s a determine from the research.

On the left hand

axis is the chance {that a} fiscal consolidation will scale back the

debt to GDP ratio, the place the common chance is 51%. The primary

column exhibits {that a} optimistic output hole (GDP is above pattern i.e. a

increase interval) turns that chance into 57%. The second column exhibits

that if the world financial system is above pattern that ratio goes from 51% to

60%. The ultimate column exhibits that if non-public credit score is excessive relative

to GDP, the chance {that a} fiscal consolidation will scale back the

debt to GDP ratio falls to 42%.

In 2010, all

economies have been recovering from recession (so the home and world

output gaps have been unfavorable) and personal credit score was excessive relative to

GDP (though falling quickly following the monetary disaster). So

2010 austerity was considerably extra prone to enhance the debt to

GDP ratio than to cut back it. As many people mentioned on the time, 2010 was

precisely the flawed time (certainly, in all probability the worst time) to embark on

fiscal consolidation, as a result of not solely would austerity decrease GDP, however

it might elevate debt to GDP as a result of decrease GDP would greater than offset

decrease debt. Which is strictly what Nationwide Institute modelling, amongst

others, mentioned

would occur again in 2011.

Some have advised

that whereas that lesson may need been related in an surroundings of

low rates of interest (the place charges can simply hit their decrease sure),

that period has just lately come to an finish. That is the place a second

piece of IMF analysis, in the identical WEO, turns into very

related. It appears at historic developments in actual rates of interest, tries

to clarify them by way of key drivers, after which assesses the place they

would possibly go sooner or later.

The underside line is

that we’ve got not entered a brand new period. As an alternative actual rates of interest are

possible to return to the identical low ranges that we noticed earlier than the

pandemic. One motive for this, demographics, is comparatively

predictable. One other is the worldwide slowdown in productiveness progress.

Productiveness progress is much less predictable, however with no decide up in sight

persevering with modest productiveness progress looks as if a superb assumption.

Except there’s something massive that’s lacking from the evaluation, the

age of low actual rates of interest (what economists name secular

stagnation) remains to be with us.

In sensible phrases

which means that the pattern degree of nominal rates of interest within the

superior economies, the extent that might neither stimulate or depress

exercise within the medium time period and the place inflation is at goal, is

between 1% and three%. That implies that as inflation falls, so will

present rates of interest. We have now not left the period when an financial

downturn may simply put rates of interest at their decrease sure. As a

outcome, it’ll stay the case that whereas financial coverage is the

first selection for controlling (extra) inflation, it’s fiscal coverage

that must be the

first selection for

avoiding recessions and boosting recoveries.

The message of this

proof is acquainted to anybody who understood macroeconomic principle

effectively earlier than 2010: go away fiscal consolidation for the nice instances. But

this can be a lesson politicians, and those who advise them, discover it

very troublesome to be taught.

So why are so many

politicians, and far of the media, so immune to accepting that

fiscal consolidations – if mandatory – ought to be reserved for good

instances and by no means undertaken in dangerous instances. A big a part of the reply

is that, for many politicians on the suitable, fiscal consolidations are

not primarily about lowering the debt to GDP ratio, however as an alternative an

excuse to chop public spending and scale back the dimensions of the state. It’s

what I’ve referred to as ‘deficit deceit’. No surprise that within the UK

over the past 13 years the federal government’s fiscal guidelines appear to alter

only a few years, as a result of they’re usually chosen to squeeze public

spending relatively than improve macroeconomic administration.

Nonetheless I don’t

suppose that’s all. The cyclical nature of the federal government’s deficit

(rising in dangerous instances, falling in good) encourages politicians to do

fiscal consolidation on the flawed time and discourage them from doing

fiscal consolidation on the proper time. [1] They do that as a result of

deficit targets deal with governments like cash-constrained people,

who if they’re wanting cash should spend much less and if they’re

flush with cash they should spend extra.

In principle this want

not occur if credible governments ditch debt targets, and guarantee

deficit targets are medium time period, like a 5 yr rolling deficit

goal. It shouldn’t occur if credible governments guarantee this

medium time period deficit goal excludes public funding, permitting

public funding to replicate social returns, authorities missions and

the price of borrowing. It shouldn’t occur if these medium time period

deficit targets are chosen intelligently, permitting debt/GDP to rise

when it is sensible to take action. And at last it shouldn’t occur if

these medium time period deficit targets are ignored if fiscal coverage is

wanted to keep away from a recession, or to stimulate the restoration from one.

That’s how wise

fiscal coverage would work. If it did, fiscal consolidation would solely

happen in good instances, and it might be efficient in lowering debt/GDP.

Fiscal consolidation wouldn’t occur in dangerous instances, permitting fiscal

stimulus to finish dangerous instances, and consolidation would solely occur in

good instances if that made financial sense.

However small state

politicians usually are not the one motive why this doesn’t occur. The

different motive is the media. Not simply the suitable wing media, that wishes

a small state, but additionally the media that likes to think about itself as

non-partisan. As I defined

right here, on the earth of mediamacro assembly deficit

targets are indicators of ‘authorities duty’, and

rolling targets that by no means arrive simply don’t wash. We have now a medium

time period rolling deficit goal right this moment, however the media nonetheless provides us

month-to-month (!) commentary on the most recent numbers for the deficit, with

predictable and countless hypothesis of tax cuts or spending cuts.

This isn’t as a result of

most journalists within the media have the flawed mannequin of how financial

coverage ought to work, however relatively they don’t have any mannequin in any respect. As a latest

BBC report implied, the principle function of a lot

journalism about financial points is financial ignorance. That’s the reason,

for instance, ministers can preserve asserting that giving medical doctors or

nurses extra money would elevate inflation with out such statements being

challenged. (Greater pay for NHS workers or academics doesn’t put

strain on costs, so it isn’t shocking that the proof

exhibits no hyperlink to inflation.) If all journalists suppose

they know is authorities deficits or debt are ‘a nasty factor’, then

this creates what I have

referred to as mediamacro.

Politicians work in

a media surroundings, so many discover it onerous to fight mediamacro. If

the media wildly inflate the significance of deficit targets, and fail

to know why these targets are rather more long run than

inflation targets, then politicians might be tempted to behave as if the

media’s view is right. Because of this deficit targets encourage

politicians to do precisely the flawed factor with fiscal coverage,

consolidating when the financial system is weak and the deficit is rising, and

enterprise fiscal growth when the financial system is robust and the

deficit is falling (or in surplus). [2]

How do you

counteract each deficit deceit from the suitable and mainstream media

ignorance? The apparent reply, as Chris

Dillow suggests, is to provide information an institutional

voice, which on this case means enhancing an impartial fiscal

council. Our personal, the OBR, was arrange by George Osborne to play a

rather more restricted position. The Treasury farmed out its fiscal

forecasting, however none of its macroeconomic evaluation. That break up makes

little financial sense, and it wants to alter.

An OBR that was ready

to offer fiscal coverage evaluation alongside its forecasts may

improve public dialogue of fiscal coverage choices, and provides area

for politicians who need to promote good coverage to counter media

ignorance. That recommendation may vary from appearing as a watchdog to cease

the federal government fiddling

the method to extra normal recommendation concerning the type of

fiscal coverage guidelines. So long as it took its lead from the educational

literature and remained impartial, this enhanced OBR would enhance

public debate about fiscal coverage, which in flip ought to assist enhance

coverage itself.

[1] Basing targets

on cyclically adjusted deficits doesn’t work, as a result of cyclical

adjustment is simply too unsure.

[2] The instance that

all the time springs to my thoughts right here is Spain

after the creation of the Euro. Spain ought to have been

working a extra restrictive fiscal coverage as a result of its inflation price

was above the Euro common, however as a result of the price range was in surplus and

due to the centrality of deficit targets within the EZ, the

political/media simply couldn’t address the thought of even bigger

surpluses.

[ad_2]