The Rebalancing Bonus - A Wealth of Frequent Sense

[ad_1]

A reader asks:

Does rebalancing primarily lock in losses? I’ve a robo suggested Roth IRA that rebalances seemingly each different day. Will I ever get again to interrupt even? And when do I cease shopping for the inventory market on sale?

Diversification is the method of spreading your bets amongst totally different asset courses, methods, geographies and holdings to cut back danger in your portfolio.

Asset allocation is the method of distilling that diversification into goal weights.

Rebalancing is the method of systematizing your purchases and gross sales to stay to that asset allocation so you’ll be able to earn the advantages of diversification.

Diversification doesn’t work with out a coherent asset allocation and asset allocation doesn’t work with out a coherent rebalancing course of.

All of them work hand-in-hand.

Rebalancing is while you trim a few of your winners to purchase a few of your losers which is a countercyclical type of investing.

Some persons are extra comfy with this technique than others however I don’t see the purpose of making an asset allocation within the first place should you don’t rebalance again to focus on weights utilizing pre-established pointers.

Let’s have a look at an instance to see how rebalancing may help your portfolio in apply.

These are the annual returns for shares (S&P 500) and bonds (10 yr treasuries) from 1928-2022:

- S&P 500 +9.6%

- 10 yr treasuries +4.6%

Should you merely took 60% of the inventory market return and 40% of the bond market return, that may get you 7.6% as a 60/40 proxy.

Everyone knows that market returns are something however common in a given yr so it may be instructive to see how rebalancing a 60/40 portfolio would have labored utilizing precise returns.

Utilizing these similar two asset courses, should you had been to rebalance again to 60/40 goal weights on an annual foundation, the 60/40 return over this similar timeframe would’ve been 8.2%.

So how will we sq. the distinction between 8.2% annual returns when rebalancing and seven.6% utilizing easy averages?

It’s the rebalancing bonus.

It doesn’t all the time work like this however it is sensible if you concentrate on it. Sure, shares have increased long-term common returns than bonds however that doesn’t all the time maintain within the short-term.

Over the previous 95 years the inventory market has outperformed the bond market in a given yr 60 occasions that means bonds have outperformed shares in 35 of these calendar years.

These years when shares do higher than bonds you’re trimming beneficial properties within the inventory market to redeploy into bonds.

And when bonds do higher than shares you’re utilizing bonds as dry powder to purchase shares whereas they’re down or underperforming.

This isn’t an ideal technique by any means however it’s a pleasant approach to preserve your self sincere as an investor.

Is every day rebalancing overkill?

Most likely.

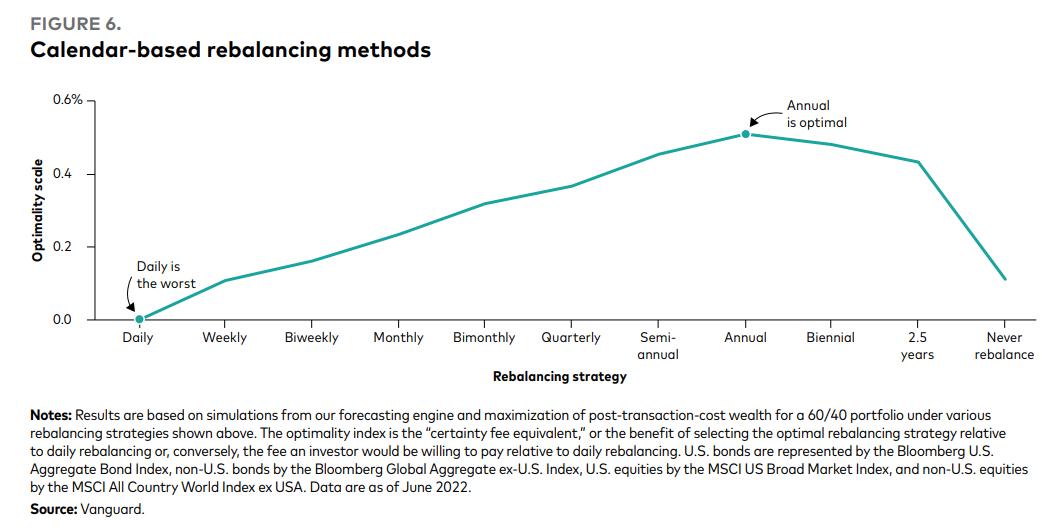

Vanguard did a deep dive on varied rebalancing intervals final yr utilizing a world 60/40 portfolio:

They discovered rebalancing too steadily or too occasionally are suboptimal methods.

The optimum interval from a danger management perspective was an annual rebalance.

The factor is you need some drift within the portfolio to permit the belongings which might be working to proceed working, no less than for a time.

Rebalancing as soon as each 6, 12 perhaps 18 months appears cheap to me.

Should you’re not comfy with a periodic solely rebalancing schedule, you possibly can additionally do some type of threshold ranges the place if an allocation will get too far out of whack you then rebalance again to focus on.

Or there may very well be some mixture of periodic rebalancing with thresholds in-between if markets get right into a crash or melt-up state of affairs.

My view on that is that it’s horseshoes and hand grenades — shut sufficient does the trick. Crucial factor with rebalancing is that you’ve got a plan of assault, persist with that plan and automate it should you can to take your self out of the equation.

As to the query of when you need to cease shopping for shares on sale — my preliminary reply is by no means.

Certain, if we’re speaking about particular person shares, a few of them are by no means getting back from the lifeless.

But when we’re speaking a couple of extra diversified subset of shares like an index fund then I really feel fairly comfy is saying that losses are non permanent and current a beautiful shopping for alternative.

I can’t supply any 100% ensures right here but when index funds crash and don’t come again we’ve got a lot greater issues to fret about than your portfolio.

One other easy approach to rebalance is by placing new contributions into your underweight positions.

And should you’re nonetheless making contributions, doing so when shares are down is an efficient factor.

You don’t need shares to get better but so long as you proceed plowing cash into them.

Try to be thrilled to be shopping for shares on sale.

We mentioned this query on the newest version of Ask the Compound the place I used to be coming dwell from stunning Montreal:

Tax skilled Invoice Candy joined me once more to debate questions on making modifications to your asset allocation, gifting cash to your youngsters, tax penalties from a pay elevate and the way taxes affect early retirement.

Additional Studying:

The Psychological Accounting of Asset Allocation

Podcast model right here:

[ad_2]