Rising labour prices have solely the smallest impression on providers inflation – William Mitchell – Fashionable Financial Concept

[ad_1]

Because the inflation episode begins to abate, central financial institution governors have been eager to advance narratives to justify why they might proceed climbing rates of interest, particularly when it’s fairly apparent that the drivers of the inflation have been largely coming from the supply-side and suppressing combination spending (through the upper charges) wouldn’t be a really efficient measure to deploy. That is fairly other than the talk as to the effectiveness of utilizing rates of interest to stifle spending, which is a separate dialogue with no clear conclusion apart from most likely not. As I’ve famous beforehand, it was onerous to argue that inflation was accelerating uncontrolled when it had began to say no many months in the past. In order that they needed to give you a distinct narrative – which was that whereas inflation was falling it was not falling rapidly sufficient. That’s the present story line the officers trot out. And that permits them to assert that if it doesn’t fall rapidly then two issues will likely be possible: (a) employees will construct the upper inflation into their wage calls for and set off a wage-price spiral that turns into self-fulfilling even after the supply-side components (Covid, Ukraine, OPEC) abate, and (b) that individuals would begin to anticipate increased inflation was the norm and construct that into the contractual preparations and pricing. Neither behavioural phenomenon has proven any signal of turning into entrenched, which leaves the central financial institution officers and not using a cowl. And even analysis from central banks themselves is demonstrating that there’s not ‘excessive inflation’ mindset taking up.

Wages progress shouldn’t be inflationary

On Tuesday (Might 30, 2023), the Federal Reserve Financial institution of San Francisco launched their newest ‘Financial Letter’ – How A lot Do Labor Prices Drive Inflation? – which addresses the wage query.

The analysis is motivated by statements made by the Federal Reserve Chair in 2022 that wage actions have been driving actions in “nonhousing providers” given they’re “the biggest value in delivering these providers”.

His assertion has been repeated often in quite a lot of alternative ways by central financial institution governors and senior officers world wide for the reason that center of 2021, when growing inflationary pressures began to emerge.

The FRBSF researcher famous that “nonhousing providers are an necessary element of general inflation, making up over half of the core private consumption expenditures (PCE) worth index.”

Additional, “Employee wages and advantages make up the majority of prices to companies” who provide these non-housing providers.

Earlier analysis has demonstrated that “labor prices have little impression on providers inflation or inflation general” as a result of companies can all the time “take in such prices into their revenue margins” and, generally, reorganise the work place to achieve productiveness boosts, which offset the upper wage prices.

The FRBSF paper framed the research by contemplating that:

… will increase in labor prices act like provide shocks, whereby companies go on increased prices to customers within the type of increased costs. In contrast, labor value progress doesn’t seem to gas inflation via increased demand.

This is a vital distinction as a result of it means that the upper incomes that employees take pleasure in because of wage will increase don’t result in extra demand conditions for items and providers.

Typically opponents to wage rises within the company sector attempt to declare that rises will likely be inflationary as a result of they are going to put stress on spending.

The FRBSF paper rejects that assertion outright.

In relation to the opposite pathway – the upper unit prices/provide impact – the analysis exhibits that:

… the impact is small and happens slowly over a very long time. A 1 proportion level (pp) improve in labor prices causes solely a 0.15pp rise within the contribution of NHS costs to core PCE inflation over a four-year horizon, which is lower than 0.04pp per 12 months. This means that the current run-up within the employment value index (ECI) is contributing solely about 0.1pp to present core PCE inflation, stemming fully from the impression on NHS inflation.

In different phrases, very small second-order kind results and never a foundation for constructing a story that rate of interest rises are justified to forestall a wage-price spiral breaking out.

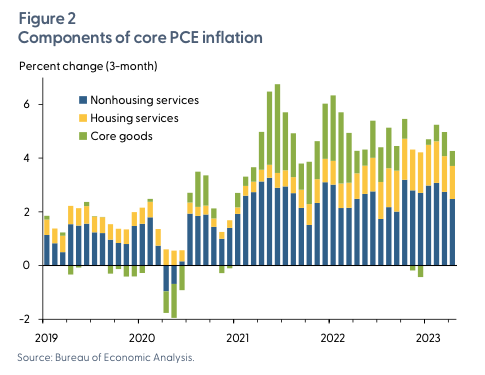

To additional the argument, the FRBSF paper produced Determine 2 (reproduced right here), which exhibits the elements of the Core PCE Inflation measure printed by the Bureau of Labor Statistics since 2019.

These elements are nonhousing providers, items and core items and the graph exhibits that Core items inflation “rose dramatically” in 2021 however has declined sharply since.

I famous in weblog posts final 12 months that this impression was simply understood within the context of the pandemic and the best way that governments handled the menace.

Not solely was the availability chain of products severely disrupted by illness and manufacturing unit and transport closures however governments additionally restricted entry to service sector actions whereas on the identical time offering pretty in depth revenue help to employees affected.

With incomes protected to some extent and no capability to have interaction in service associated spending, it was apparent that the diverted spending on items – house enhancements, introduced ahead purchases, and so forth – would push up costs of these commodities particularly as they have been in comparatively quick provide in 2020 and 2021.

To name that an extra demand inflation is true in a strict sense however from a coverage perspective such a diagnose has led to harmful insurance policies from central banks and treasuries.

It was clear that the general spending didn’t develop that a lot and that the issue was the ‘momentary’ discount in provide functionality.

So it was higher taking the Japanese route and ready for the availability aspect to resolve whereas on the identical time defending essentially the most deprived households from the momentary cost-of-living stress with fiscal injections.

Utilizing macroeconomic coverage to kill off spending would simply depart a legacy of upper unemployment and misplaced incomes as the availability aspect overcome its constrained atmosphere.

The graph exhibits how that a part of the story resolved itself largely by the center of 2022.

Conversely, nonhousing providers elevated its contribution and maintained the extent over the course of the inflation cycle.

The FRBSF paper calculates that:

NHS is contributing 2.4pp to three-month core inflation, which is 1pp bigger than its 2016–19 common contribution.

And since nominal wages progress has elevated over this era – chasing the CPI actions – many commentators are blaming that motion on the general PCE motion.

The FRBSF analysis examines the connection between actions within the Employment Value Index (ECI), the most effective measure of labour prices and NHS inflation over the interval 1988 to 2023, utilizing quarterly information.

So it makes use of adequate information observations to estimate a sturdy econometric mannequin and achieve sound inference.

Curiously (from an econometrics perspective), they discover no vital distinction within the relationship once they cut up the pattern into two at round 2020.

So the connection within the present interval behaves equally to the pre-pandemic interval, regardless of the extraordinary nature of the pandemic.

The primary outcomes they report are:

1. The impression of ECI will increase on Items and Housing Companies inflation is negligible and never statistically totally different from zero.

2. The impression on NHS is constructive and statistically vital however “the magnitude is kind of small”.

3. “As ECI progress has elevated by about 3pp from its pre- pandemic degree, which means that labor prices have added roughly 0.1pp to present core PCE inflation.”

So actually nothing to see right here!

The opposite problem they explored was whether or not this minuscule wages impact labored through the supply-side (pushing up prices which companies go on) or demand-side (increased spending impact), which I discussed above.

The analysis concludes that:

The ECI has no discernible impact on the demand-driven element of NHS inflation. As a substitute, the impression of ECI progress on NHS inflation stems fully from the supply-driven element. Thus, this end result signifies that will increase in labor prices act like typical provide shocks, whereby companies go increased prices alongside to customers within the type of increased costs.

However as famous beforehand, this impact is small.

Importantly, they observe that:

… current proof exhibits that wage progress tends to comply with inflation … [and] … that current labor-cost progress is prone to be a poor gauge of dangers to the inflation outlook.

That is vital analysis.

I’ve famous up to now that whenever you observe actual wages declining it’s onerous to mount a case that wages are driving inflation.

The FRBSF analysis helps that declare – that nominal wages progress is chasing the inflation however not catching up or overtaking it.

Which then leaves us to counsel that the inflation now, as these Core Items provide pressures are abating quick, is being pushed by margin push – the so-called ‘greedflation’.

That now stands as a extremely believable rationalization for the ‘persistent’ of the inflationary pressures into 2023.

RBA governor nonetheless blames wages

Yesterday, the RBA governor appeared earlier than the Commonwealth Senate Estimates Committee.

The transcript continues to be not accessible.

However we have now a superb set of quotes from his look.

He claimed that actual wages must proceed falling in Australia to ensure that inflation to get again to the RBA’s goal vary of two to three per cent as a result of productiveness progress had stalled.

In different phrases, he was in not so many phrases, suggesting that the RBA would intentionally drive the financial system into recession with a view to obtain additional declines in actual wages.

Within the March-quarter 2019, the actual wage index (derived from the ABS Wage Worth Index) stood at 113.1, which was the newest peak.

That indicated that actual wages had solely progress by 13.1 per cent for the reason that September-quarter 1997, when the WPI information sequence started.

By comparability, over the identical interval, GDP per hour of labour enter (productiveness) had grown by 29.6 per cent, which means that over this 2 decade or extra interval, nationwide revenue had been massively redistributed away from employees to earnings

The related measure is the wage share and that moved from 55 per cent within the September-quarter 1997 to 50 per cent within the December-quarter 2022.

An unprecedented shift to earnings.

Which means in plain language that employees actual wages haven’t progress in proportion to productiveness progress and the hole has been pocketed by enterprise companies.

Within the March-quarter 2023, the actual wage index stood at 107.2 factors whereas the productiveness index had grown from 129.6 factors to 131.8 factors.

So actual wages have declined over this era (March-quarter 2019 to March-quarter 2023) by 5.1 factors and labour productiveness has grown by 1.7 factors.

Certain sufficient, the productiveness progress has been very low by historic requirements.

However nonetheless, employers have discovered methods to take advantage of the inflationary interval to suppress actual wages but nonetheless pocket good points from labour productiveness through elevated revenue margins.

So when the RBA governor claims that the one means actual wages can rise is thru productiveness progress, he isn’t telling us the complete story.

Even with the parlous productiveness progress the Australian financial system is producing at current, there’s scope for non-inflationary actual wage will increase if we power the companies to desist from profit-gouging.

That’s, there’s scope to scale back revenue margins from their inflated ranges which have allowed the revenue share to increase.

Conclusion

Nevertheless, don’t anticipate the RBA governor to articulate that message any time quickly.

As I famous yesterday, the governor mislead the Senate Committee when he claimed the one revenue will increase have been within the sources sector.

That was clearly not a press release that may be supported by the info.

That’s sufficient for at this time!

[ad_2]