RIA Code Of Ethics: Necessary Nuances To Notice In Comparatively Simple Necessities

[ad_1]

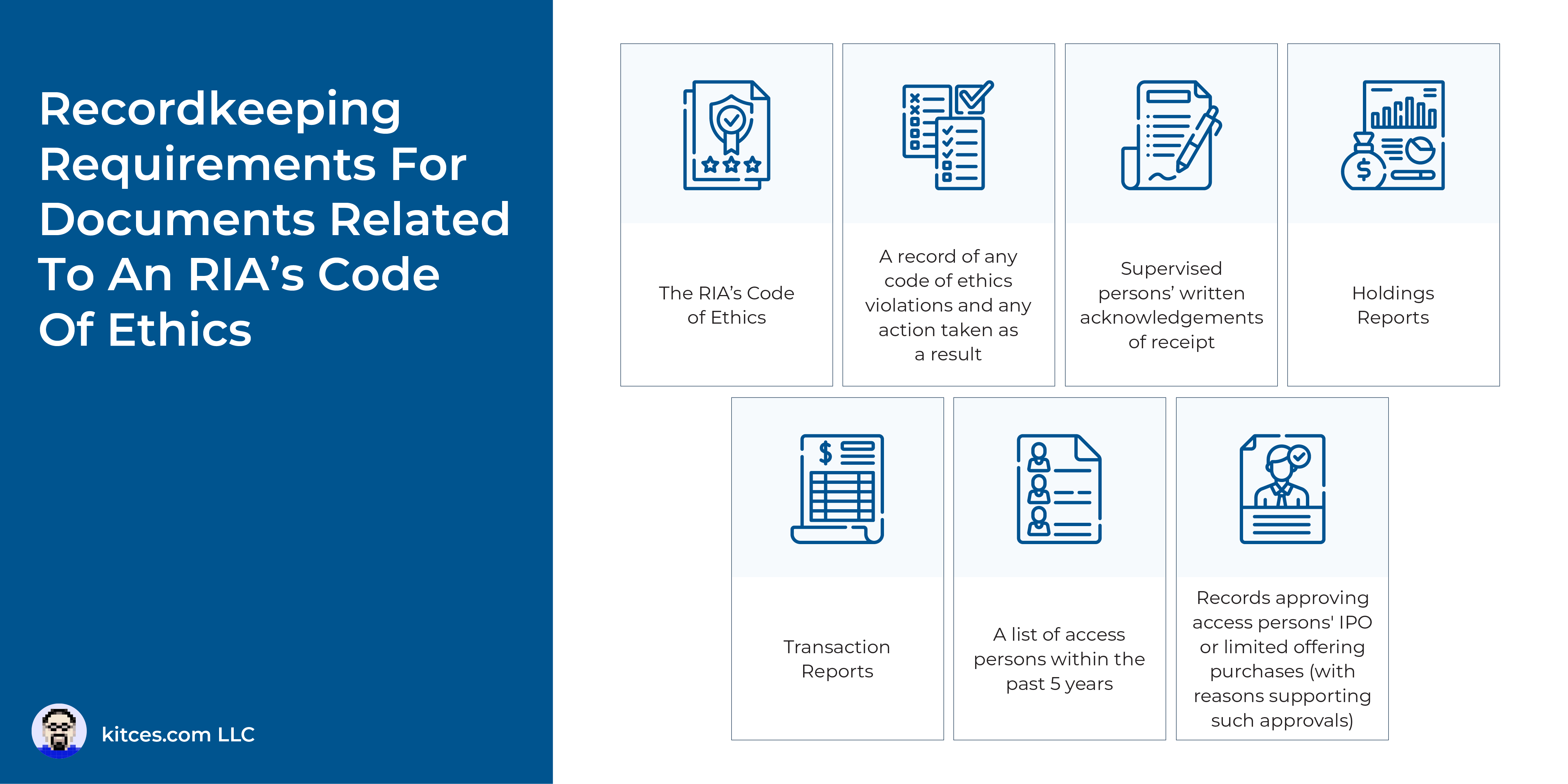

All funding advisers are fiduciaries that owe an obligation of care and loyalty to their shoppers, and, in a really perfect world, advisory companies and their employees would abide by these necessities with out the necessity for a prescriptive code of ethics. Nevertheless, the early 2000s had been stricken by a wide range of SEC enforcement actions that alleged fiduciary obligation violations – primarily involving buying and selling abuses by funding advisory personnel – which led the regulator to create a rule (that grew to become efficient in 2004) requiring all SEC-registered funding advisers to undertake and implement a written code of ethics relevant to its supervised individuals. The SEC’s Funding Adviser Codes of Ethics Rule requires all SEC-registered funding advisers to determine, preserve, and implement a written code of ethics that, at a minimal, consists of 5 areas: 1) itemizing requirements of enterprise conduct; 2) complying with relevant Federal securities legal guidelines; 3) requiring entry individuals to report their private securities transactions and holdings for evaluation; 4) reporting violations; and 5) distributing and acknowledging receipt of the agency’s code of ethics. Whereas a lot of the Rule’s necessities are comparatively easy, there are detailed nuances that IAR advisers should be aware of to implement their very own codes of ethics pursuant to the SEC’s rule.

As a place to begin, funding advisers should deal with 3 essential questions when designing and implementing a compliant code of ethics: who throughout the agency is topic to reporting their private securities transactions; what data must be reported; and when this data should be reported. “Entry individuals” are outlined as “supervised individuals” with entry to nonpublic data concerning any shoppers’ buy or sale of securities or concerning the portfolio holdings of any reportable fund, or is concerned in making securities suggestions to shoppers, or who has entry to such suggestions which can be nonpublic. Such people are required to submit each holdings stories (inside 10 days of first being deemed an entry particular person and a minimum of as soon as in every 12-month interval) in addition to transaction stories (inside 30 days of the tip of every calendar quarter) for reportable securities that they or quick relations beneficially personal. Notably, these are simply minimal necessities for the agency’s code of ethics and the SEC means that companies think about different areas for potential inclusion (e.g., “Blackout intervals” when consumer securities trades are being positioned or suggestions are being made and entry individuals aren’t permitted to put their very own private securities transactions).

Along with amassing the required stories, the agency’s Chief Compliance Officer (CCO) additionally has sure evaluation necessities. For example, the CCO ought to be looking out for entry individuals who’re putting their very own pursuits forward of shoppers, usurping consumer funding alternatives for their very own private profit, or in any other case managing their very own private investments in such a method that doesn’t replicate their fiduciary duties to shoppers.

Finally, the important thing level is that an funding adviser’s code of ethics isn’t just a professional forma doc, however moderately a key a part of making certain that the agency resides as much as its fiduciary obligation to its shoppers. Which not solely units expectations concerning ethics for the agency’s management and employees, but in addition provides potential and present shoppers extra confidence within the degree of care they will count on to obtain when working with the agency!

Learn Extra…

[ad_2]