Keep away from These 5 Huge Tax Errors with RSUs, Inventory Choices, and ESPP

[ad_1]

Inventory compensation generally is a nice pathway to wealth, however in addition they include their very own set of tax implications. Sadly, many taxpayers miss vital tax concerns in terms of inventory compensation.

On this submit, we’ll discover the highest 5 issues which might be usually missed in terms of taxes and inventory compensation, together with:

If you happen to can keep away from even one in every of these errors, you would possibly save $1000s in taxes and costs to a tax advisor to re-do incorrectly executed tax returns…to not point out a big trouble.

[Flow’s Note: This post was written by guest blogger John McCarthy. John’s firm, McCarthy Tax Preparation, is a tax preparation and planning firm that has been serving clients since 2001. Their mission is to help technology employees with proactive tax planning for their equity compensation. Learn more about John and his firm, or schedule an introductory call.]

A “Transient” Abstract of Inventory Compensation Tax Reporting

The surest technique to get your self in scorching water with the IRS is to not report inventory choices accurately in your tax return. Every sort of inventory compensation is dealt with in a different way, so it’s vital to know what reporting you’re answerable for.

Let’s check out the tax remedy at varied phases:

| TYPE OF STOCK COMPENSATION | STAGE 1: GRANT (when shares are awarded to you; often they’re not yours but) |

STAGE 2: VEST | STAGE 3: EXERCISE/PURCHASE | STAGE 4: SALE |

| Worker Inventory Buy Plan (ESPP) | The beginning of the Providing IntervalNo tax reporting | Throughout the Buy Interval

No tax reporting |

On the finish of the Buy Interval, when shares are robotically bought for you.

No tax reporting |

Both Atypical Revenue or Capital Good points |

| Restricted Inventory Models (RSU) | No tax reporting | When the RSUs flip into shares of inventory for you

Atypical Revenue in your paystub and tax withholding |

n/a | Capital Achieve or Loss |

| Non-Certified Inventory Choices (NQSO) | No tax reporting | When the choices vest, you are actually permitted, not obligated, to train them to personal a share of inventory

No tax reporting |

If you pay the strike worth to show the choice right into a share of inventory you personal

Atypical Revenue in your paystub and tax withholding |

Capital Achieve or Loss |

| Incentive Inventory Choices (ISO) – Disqualified Disposition (offered earlier than one 12 months of train or two years from grant) | No tax reporting | When the choices vest, you are actually permitted, not obligated, to train them to personal a share of inventory

No tax reporting |

If you pay the strike worth to show the choice right into a share of inventory you personal

Atypical Revenue in your paystub (no tax withholding) |

Capital Achieve or Loss |

| Incentive Inventory Choices (ISO) – Certified Disposition | No tax reporting | When the choices vest, you are actually permitted, not obligated, to train them to personal a share of inventory

No tax reporting |

If you pay the strike worth to show the choice right into a share of inventory you personal

Doable Different Minimal Tax (AMT) |

Capital Achieve or Loss & AMT Credit score |

| Restricted Inventory – 83(b) election (rationalization under) | Atypical Revenue added to your 1040 (i.e., not in your paystub, no tax withholding) | No tax reporting | No tax reporting | Capital Achieve or Loss |

As you’ll be able to see, there are various tax reporting necessities, and reporting could be fairly a bit completely different relying on what sort of inventory compensation you obtain.

Usually, the IRS desires their share every time there was a switch of worth to you.

At grant and at vesting, there’s usually no additional motion that it is advisable to take in your return, with one exception:

83(b) Election (“Early Train”)

If you happen to’ve acquired Restricted Inventory (generally known as “founder inventory”, very low-value inventory usually given to early staff at a start-up) you could wish to take into account an 83(b) election. An 83(b) election permits you to report earnings at a presumably (hopefully) a lot decrease worth and begins the clock on decrease capital beneficial properties charges.

Timing is vital right here, as a result of the IRS requires this election inside 30 days of you receiving this inventory. 83(b) elections are outdoors the scope of this text, so please make sure you see your tax advisor if this is applicable to you.

Which takes us to the primary generally missed merchandise…

Mistake #1: Not Reporting Capital Good points (or Losses) on the Sale of Inventory

Because the chart above signifies, it’s essential to at all times report gross sales when inventory is offered.

Folks usually get confused in regards to the taxes and withholding on the vesting or train and the way that impacts the reporting when the shares are offered. Shoppers usually assume that as a result of taxes had been already withheld, nothing must be reported to the IRS on the sale. This ends in tons of notices and correspondence from the IRS.

The IRS receives a Type 1099 reporting doc from the corporate (ex. Shareworks, Constancy, and many others) that holds your choices. This doc stories the full gross proceeds from the sale, however is commonly lacking the worth of the inventory compensation that was already included in your W2 as earnings, aka your “value foundation.”

Consequently, the IRS expects to see a big achieve reported from the sale, till you inform them in any other case. This is the reason reporting your inventory gross sales on Schedule D of your return is so essential.

That is the place you inform the IRS that you simply’ve already paid taxes on these choices (by way of payroll tax withholding), by making an adjustment to the price foundation reported on the Schedule D. You might be subtracting your value foundation from the gross sales proceeds, which reduces your taxable achieve. This lowers your tax invoice.

Talking of value foundation…

Mistake #2: Double Counting Revenue

Keep in mind these 1099s we simply talked about?

Most of the time, they present the incorrect value foundation. If you happen to take this data straight from the 1099 reporting type, you threat paying double the tax on the sale of this type of inventory compensation:

- RSUs

- NSOs, and

- ISO shares that you simply’ve owned for lower than a 12 months

Why can’t we depend on the 1099s issued?

Get this, the IRS prohibits brokers (like Shareworks, Constancy) from together with the compensation earnings acknowledged by the worker in the price foundation reported on Type 1099-B.

So the IRS is actively making it tougher so that you can file your tax return. Nice. Simply Nice.

The bit of excellent information right here is that the majority brokers make it comparatively straightforward to seek out the data wanted to keep away from double paying tax in your possibility gross sales. Buried someplace within the tax doc part of your portal, you need to see a doc known as “Supplemental Tax Data”. Make sure you obtain this and embrace it along with your tax paperwork. Your tax professional goes to wish it.

And should you’ve found a mistake on a previous return, remember you have got three years from the due date of the return to file a correction or amended return. We will’t rely the variety of these we’ve executed for shoppers on this actual scenario.

So…what about ISOs?

Mistake #3: Forgetting about Different Minimal Tax on ISOs

In our desk above you’ll be able to see that, typically, any tax penalties at train are dealt with by way of your organization’s payroll. The exception could be Incentive Inventory Choices.

ISOs will usually set off Different Minimal Tax (“AMT”) should you maintain your shares for one 12 months after train (a professional disposition).

What’s AMT? The Different Minimal Tax (AMT) is a separate tax system designed to make sure that individuals with larger earnings pay a minimal quantity of taxes.

It was initially created to forestall rich taxpayers from utilizing deductions and credit to cut back their tax legal responsibility to zero. The AMT has a separate algorithm and exemptions, and taxpayers should calculate their legal responsibility below each the common tax system and the AMT to find out which is larger.

One of many huge variations between Common and AMT tax computation is the remedy of ISOs.

If you train an ISO, you’re deemed to have acquired worth (earnings) for the distinction between the present honest market worth (in a non-public firm, that is the 409(a) worth) and the strike worth (aka, train worth) of the shares. It’s important to report this earnings on Type 6251 for AMT functions, regardless that you haven’t offered (or couldn’t promote) the shares from exercising choices.

Take into account that there isn’t a withholding tax once you train ISOs.

You wish to be doubly positive of the tax penalties of exercising ISOs earlier than you train. We’ve seen shoppers with six-figure AMT tax payments which might be restricted from promoting the shares in pre-IPO corporations.

So, what occurs to all that AMT tax once you promote shares? I’m so glad you requested…

Mistake #4: Forgetting in regards to the AMT Tax Credit score

If there’s any excellent news about paying AMT tax up-front on the train of your ISOs, it’s that you simply get to hold ahead an AMT tax credit score that can be utilized once you promote your shares. (You’ll be able to even use a small portion of the credit score in years once you don’t promote ISOs, so long as your AMT tax is lower than your Common tax for the 12 months.)

Keep in mind once we talked about value foundation above? And the way it’s straightforward to report the inaccurate quantity of value foundation on inventory choices? Nicely…. ISOs don’t make issues any simpler, I’m afraid.

ISOs have a Common Value Foundation and an AMT Value Foundation.

Let that sink in a second.

Because of this it is advisable to monitor each value bases as a result of your Common tax achieve is computed in a different way out of your AMT tax achieve. This additionally implies that within the 12 months of sale, your AMT value foundation on a professional disposition (shares held a couple of 12 months previous train) is usually lower than your Common value foundation.

When your AMT tax is lower than your Common tax, the distinction frees up AMT tax credit that you simply generated within the 12 months of train. Any AMT tax credit score that isn’t in a position for use will get reported on IRS Type 8801 within the 12 months after your train.

After we see errors on this space, it’s usually the results of switching tax preparation software program (or switching tax preparers) from 12 months to 12 months.

With out your prior 12 months tax data, it may be very straightforward to overlook AMT tax credit, particularly if the quantities are usually not very massive relative to your different earnings.

And, should you’ve made it this far into the weeds with inventory choices, Congratulations! Right here is without doubt one of the most vital errors of inventory compensation…

Mistake #5: Massive Balances Due (and Curiosity and Penalties) at Tax Submitting Time

After talking with a whole bunch of inventory compensation shoppers through the years, the commonest chorus we hear (and why they’re in search of out assist for the primary time) is a shock steadiness due at return time.

In spite of everything, it looks like a ton of taxes are taken out of your paycheck already. Why is there nonetheless such a big steadiness due in your tax return?

Let’s check out an instance:

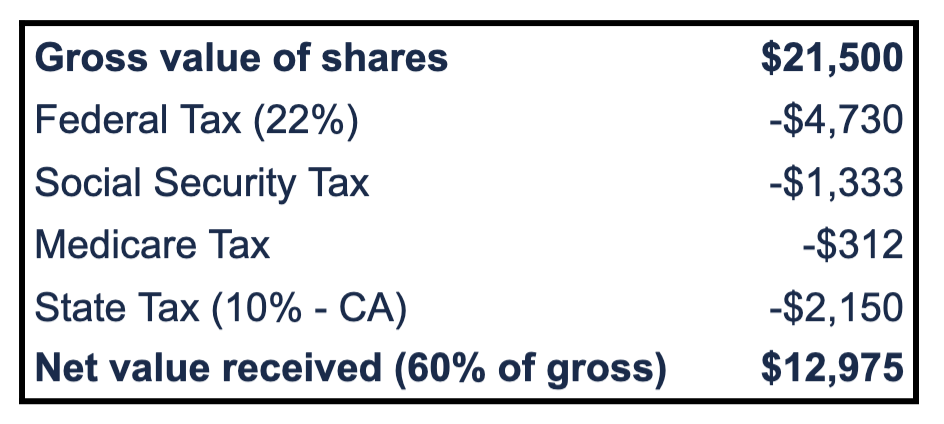

Alice has quarterly vesting of RSUs at Apple and receives 100 shares valued at $215/share in Feb 2023. Alice’s wage is $350,000/ 12 months, submitting as single.

Alice’s paystub reveals the next:

Alice could also be saying, “I already paid 40% tax on my shares, how is it doable that I owe extra at tax time?!”

The hot button is that of the 40% withholding, solely 22% goes in the direction of Federal earnings tax.

And Alice is making $350,000 per 12 months so she is within the 35% efficient tax bracket. Alice is underwithheld on these RSUs by about 13%, which implies a tax invoice of one other $2,795 come return time.

If you happen to don’t funds for this, it may be an enormous blow at return time.

To make issues worse, should you obtain different varieties of compensation—like bonuses, commissions, and many others. (something apart from wage)—the IRS additionally requires employers to withhold federal earnings taxes at 22%.

The IRS considers all these varieties of compensation “Supplemental Compensation” and requires employers to withhold at a flat 22% regardless of the tax withholding elections you have got in place along with your payroll division in your wage. (Word: this withholding price jumps to the highest price of 37% as soon as your compensation is over $1MM for the 12 months.)

Some tech corporations are permitting their staff to elect a better tax withholding price on supplemental compensation.

Electing a better tax withholding price on RSUs, bonuses, and many others., may also help you keep away from each a big tax invoice at return time and the necessity to make quarterly estimated tax funds (that are a trouble, arduous to compute, and simple to neglect).

You could solely have one shot to select this price initially of the tax 12 months, so watch fastidiously for any communication out of your payroll division and work along with your tax skilled to find out the correct stage of withholding.

And a ultimate notice about curiosity and penalties…

You will need to perceive your full 12 months tax legal responsibility as a result of the IRS will count on you to pay the correct quantity of tax all year long

To keep away from curiosity and penalties, it is advisable to meet the decrease of the next “secure harbors”:

- Pay 110% of prior 12 months tax legal responsibility, or

- Pay 90% of present 12 months tax legal responsibility

Most states have related guidelines, however verify your state to make certain.

If you happen to haven’t paid sufficient all year long, the IRS can assess underpayment penalties and curiosity. You’ll be able to simply keep away from this with the correct tax planning.

Tax reporting for inventory compensation is just not for the faint of coronary heart, however with the correct planning you’ll be able to keep away from the commonest errors talked about above.

If you happen to’re new to inventory compensation, please make sure you do your analysis or attain out to a professional tax skilled who usually works with stock-compensation shoppers for assist.

If you wish to work with a monetary planner who may also help you make tax-aware choices, and who may also help join you with different knowledgeable professionals (like CPAs!), attain out and schedule a free session or ship us an electronic mail.

Join Circulate’s twice-monthly weblog electronic mail to remain on prime of our weblog posts and movies.

Disclaimer: This text is supplied for academic, common data, and illustration functions solely. Nothing contained within the materials constitutes tax recommendation, a advice for buy or sale of any safety, or funding advisory providers. We encourage you to seek the advice of a monetary planner, accountant, and/or authorized counsel for recommendation particular to your scenario. Replica of this materials is prohibited with out written permission from Circulate Monetary Planning, LLC, and all rights are reserved. Learn the complete Disclaimer.

[ad_2]