Australia nationwide accounts – financial progress slumps to under 1 per cent annualised – unemployment on the rise

[ad_1]

The Australian Bureau of Statistics launched the newest – Australian Nationwide Accounts: Nationwide Earnings, Expenditure and Product, March 2023 – at the moment (March 1, 2023), which exhibits that the Australian economic system grew by simply 0.2 per cent within the March-quarter 2023 and by 2.3 per cent over the 12 months. If we lengthen the March outcome out over the 12 months then GDP will develop by 0.8 per cent, nicely under the speed required to maintain unemployment from falling. Working hours dropped within the March-quarter and I anticipate that pattern to speed up within the coming quarters given the conduct of the central financial institution and treasury. The March-quarter outcome represents a major decline in progress, Households in the reduction of additional on consumption expenditure whereas on the identical time saving much less relative to their disposable earnings in an effort to keep up consumption progress within the face of rising rates of interest and short-term inflationary pressures. I anticipate progress to say no additional and we can be left with rising unemployment and declining family wealth because of the RBA’s poor judgement.

The primary options of the Nationwide Accounts launch for the March-quarter 2023 had been (seasonally adjusted):

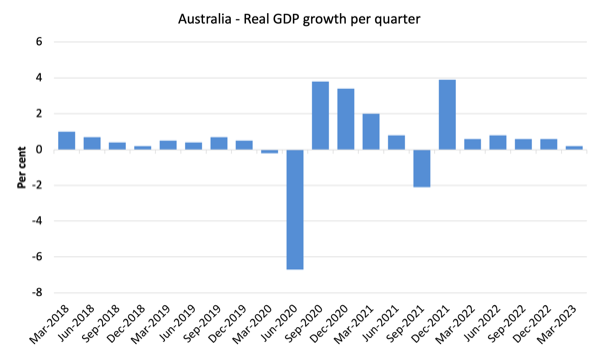

- Actual GDP elevated by 0.2 per cent for the quarter (down from 0.5 per cent final quarter). The annual progress fee was 2.3 per cent however the annualised March-quarter fee would solely be 0.8 per cent – heading in direction of recession.

- Australia’s Phrases of Commerce (seasonally adjusted) rose by 2.8 per cent and by 0.1 per cent over the 12 month interval.

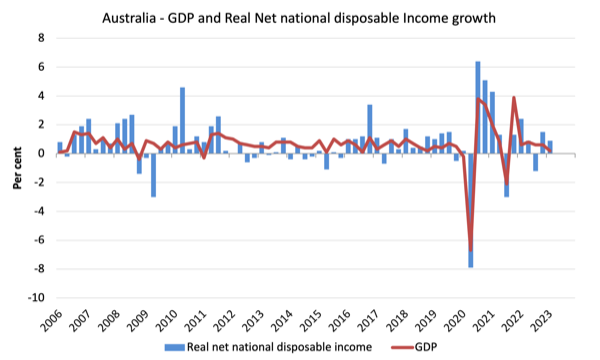

- Actual web nationwide disposable earnings, which is a broader measure of change in nationwide financial well-being, rose by 0.9 per cent for the quarter and by 2.1 per cent over the 12 months, which signifies that Australians are higher off (on common) than they had been at that time 12 months in the past.

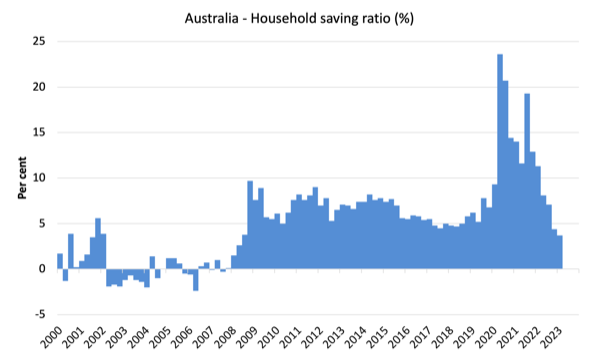

- The Family saving ratio (from disposable earnings) fell to three.7 per cent from 4.4 per cent. So the squeeze on family wealth is having an impact with consecutive declines within the ratio.

General progress image – progress continues at a lot slower fee

The ABS – Media Launch – mentioned that:

Australian gross home product (GDP) rose 0.2 per cent (seasonally adjusted, chain quantity measure) within the March quarter 2023 and by 2.3 per cent in comparison with March quarter 2022 …

That is the sixth straight rise in quarterly GDP however the slowest progress because the COVID-19 Delta lockdowns in September quarter 2021 …

Non-public and public gross fastened capital formation had been the primary drivers of GDP progress this quarter …

Family spending continued to gradual within the March quarter 2023 …

The family saving to earnings ratio fell to three.7 per cent, its lowest stage since June quarter 2008 …

Web commerce detracted 0.2 proportion factors from GDP, as exports elevated 1.8 per cent and imports rose 3.2 per cent.

The primary graph exhibits the quarterly progress during the last 5 years.

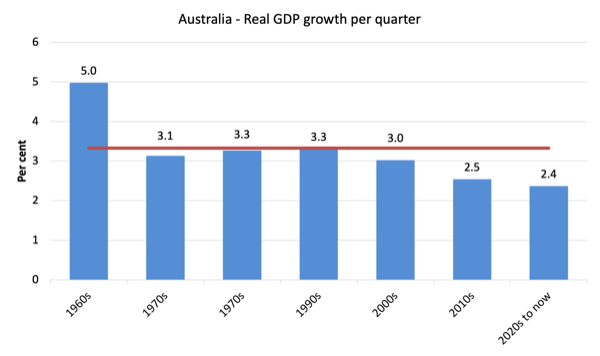

To place this into historic context, the subsequent graph exhibits the last decade common annual actual GDP progress fee because the Nineteen Sixties (the horizontal crimson line is the typical for the complete interval (3.26 per cent) from the March-quarter 1960 to the March-quarter 2008).

The 2020-to-now common has been dominated by the pandemic.

However, it is usually apparent how far under historic traits the expansion efficiency of the final 2 a long time have been because the fiscal surplus obsession has intensified on either side of politics.

Even with a large family credit score binge and a once-in-a-hundred-years mining increase that was pushed by stratospheric actions in our phrases of commerce, our actual GDP progress has declined considerably under the long-term efficiency.

The Nineteen Sixties was the final decade the place authorities maintained true full employment.

Evaluation of Expenditure Parts

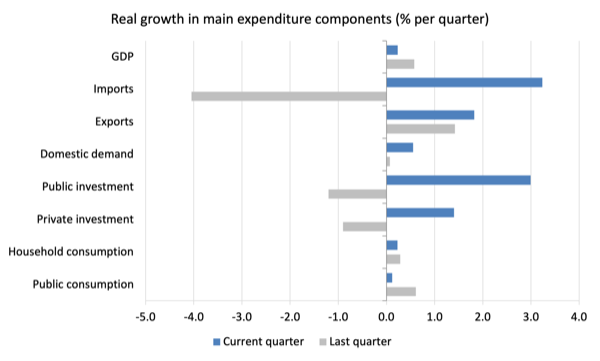

The next graph exhibits the quarterly proportion progress for the main expenditure elements in actual phrases for December-quarter 2022 (gray bars) and the March-quarter 2023 (blue bars).

Factors to notice for the March-quarter:

1. Family Consumption expenditure rose by simply 0.23 per cent (down from 0.29 per cent) – spending progress has now declined for the final three quarters on the identical time that family saving is being rundown to assist the present declining progress.

2. Basic authorities consumption expenditure rose by 0.12 per cent (down from 0.61 per cent). Recurrent authorities spending now tightening as nicely.

3. Non-public funding expenditure progress rose by 1.4 per cent after declining by 0.9 per cent within the final quarter.

4. Public funding rose by 2.99 per cent on the again of huge state and native authorities infrastructure tasks.

5. Export expenditure rose by 1.8 per cent. Imports progress was 3.2 per cent).

6. Actual GDP rose by simply 0.23 per cent (down from 0.6 per cent).

Contributions to progress

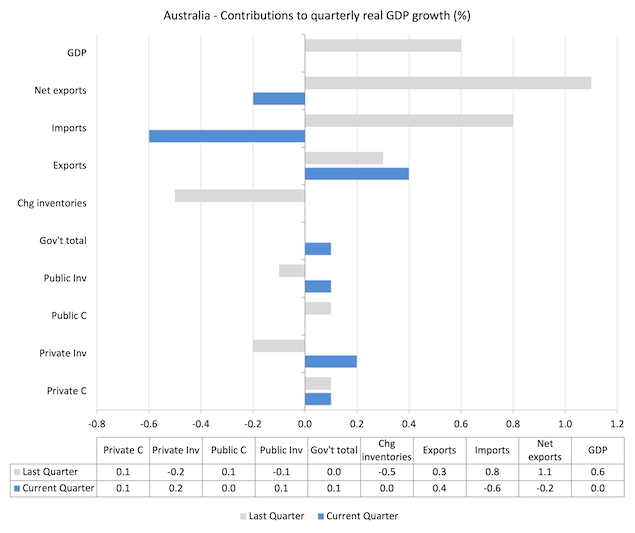

What elements of expenditure added to and subtracted from the 0.2 per cent rise in actual GDP progress within the March-quarter 2023?

The next bar graph exhibits the contributions to actual GDP progress (in proportion factors) for the primary expenditure classes. It compares the March-quarter 2023 contributions (blue bars) with the earlier quarter (grey bars).

In no order:

1. Family consumption expenditure added 0.1 factors to the general progress fee (regular).

2. Non-public funding expenditure added 0.2 factors (after subtracting 0.2 factors final quarter).

3. Public consumption added 0.0 factors this quarter after including 0.1 factors final quarter.

4. Public Funding added 0.1 level this quarter (after subtracting 0.1 factors final quarter).

5. General, the federal government sector added 0.1 level to progress (after including nothing final quarter).

6. Progress in inventories added nothing (after subtracting 0.5 factors final quarter).

7. Web exports subtracted 0.2 factors to progress with exports (+0.4 factors) being overridden by rise in imports (-0.6 factors) – keep in mind imports are a drain on expenditure.

Materials dwelling requirements rose modestly in March-quarter

The ABS inform us that:

A broader measure of change in nationwide financial well-being is Actual web nationwide disposable earnings. This measure adjusts the quantity measure of GDP for the Phrases of commerce impact, Actual web incomes from abroad and Consumption of fastened capital.

Whereas actual GDP progress (that’s, whole output produced in quantity phrases) rose by 0.2 per cent within the March-quarter, actual web nationwide disposable earnings progress rose by 0.9 per cent.

How will we clarify that?

Reply: The phrases of commerce rose from 0.3 per cent within the December-quarter to 2.8 per cent for the quarter.

The ABS famous that “The autumn in import costs was pushed by the worldwide fall in oil costs and the appreciation of the Australian greenback. This was the biggest quarterly fall in import costs since December 2010. The autumn in export costs was led by rural and mining commodities.”

Family saving ratio fell by 0.7 factors to three.7 per cent

The ABS famous that:

The family saving to earnings ratio fell to three.7 per cent, its lowest stage since June quarter 2008 … This was pushed by increased earnings tax payable and curiosity payable on dwellings, and elevated spending because of the rising value of dwelling pressures … Family consumption grew quicker this quarter than the rise in gross disposable earnings.

With inflation quickly at elevated ranges and rates of interest now being pushed up by the RBA, the squeeze on earnings is seeing households sustaining (moderating) progress in consumption expenditure by lowering their saving fee.

Digging into financial savings to keep up the move of consumption spending undermines family wealth and is a finite course of, particularly given the document ranges of family debt.

The next graph exhibits the family saving ratio (% of disposable earnings) from the March-quarter 2000 to the present interval. It exhibits the interval main as much as the GFC, the place the credit score binge was in full swing and the saving ratio was detrimental to the rise in the course of the GFC after which the newest rise.

The present place is that households are being squeezed by a mix of rising dwelling prices and rates of interest and flat wages progress, which is driving a niche between earnings and expenditure.

If this pattern continues, Australia will return to the pre-GFC interval when the family saving ratio was detrimental and consumption progress was sustained by rising debt.

Nevertheless, with family debt so excessive, it’s seemingly that households will in the reduction of consumption spending and the economic system will head in direction of recession.

Will probably be a deliberate act of sabotage engineered by the RBA.

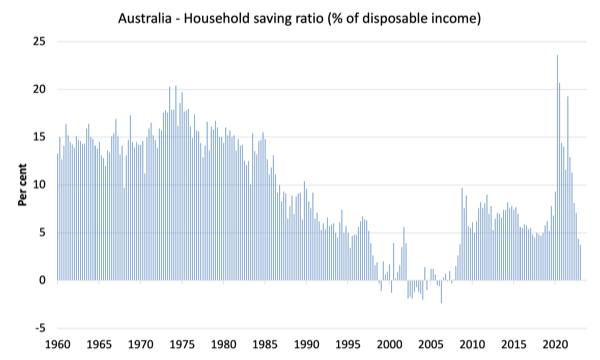

The subsequent graph exhibits the family saving ratio (% of disposable earnings) from the March-quarter 1960 to the present interval.

Again within the full employment days, when governments supported the economic system and jobs with steady fiscal deficits (principally), households saved vital proportions of their earnings.

Within the neoliberal interval, as credit score has been rammed down their throats, the saving fee dropped (to detrimental ranges within the lead-up to the GFC).

Hopefully, households are paying off the document ranges of debt they’re now carrying and enhancing their monetary viability.

The next desk exhibits the affect of the neoliberal period on family saving. These patterns are replicated all over the world and expose our economies to the specter of monetary crises far more than in pre-neoliberal a long time.

The outcome for the present decade (2020-) is the typical from March 2020.

| Decade | Common Family Saving Ratio (% of disposable earnings) |

| Nineteen Sixties | 14.4 |

| Seventies | 16.2 |

| Nineteen Eighties | 11.9 |

| Nineteen Nineties | 5.0 |

| 2000s | 1.4 |

| 2010s | 6.5 |

| 2020- | 12.3 |

Actual GDP progress rose however working hours fell

Actual GDP rose 0.2 factors within the quarter, whereas working hours fell by 0.8 per cent.

The ABS report that GDP per hours labored fell (though the earlier sentence would indicate that productiveness rose). So there’s something fishy with the information right here and I anticipate subsequent quarter revisions will happen.

The next graph presents quarterly progress charges in actual GDP and hours labored utilizing the Nationwide Accounts information for the final 5 years to the March-quarter 2023.

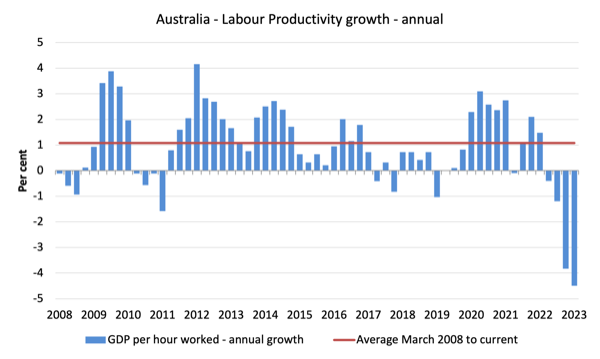

To see the above graph from a distinct perspective, the subsequent graph exhibits the annual progress in GDP per hour labored (labour productiveness) from the March-quarter 2008 quarter to the March-quarter 2023. The horizontal crimson line is the typical annual progress since March-quarter 2008 (1.1 per cent), which itself is an understated measure of the long-term pattern progress of round 1.5 per cent every year.

The comparatively sturdy progress in labour productiveness in 2012 and the principally above common progress in 2013 and 2014 helps clarify why employment progress was lagging given the true GDP progress. Progress in labour productiveness signifies that for every output stage much less labour is required.

GDP per hours labored has now fallen for the final four-quarters – a poor final result.

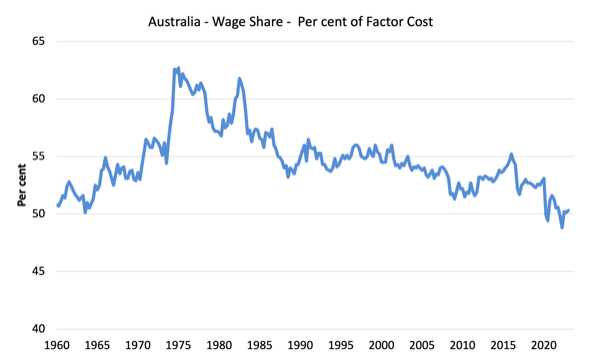

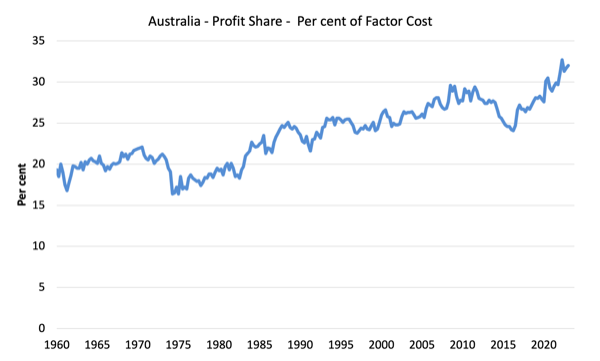

The distribution of nationwide earnings – principally steady

The wage share in nationwide earnings rose barely to 50.3 per cent whereas the revenue share rose by 0.3 factors because the phrases of commerce improved and companies recorded document revenue ranges.

The share of different claimants (similar to authorities) thus declined barely.

However as the next graphs present, this shift is minor within the face of the latest traits.

The primary graph exhibits the wage share in nationwide earnings whereas the second exhibits the revenue share.

The declining share of wages traditionally is a product of neoliberalism and can in the end need to be reversed if Australia is to take pleasure in sustainable rises in requirements of dwelling with out document ranges of family debt being relied on for consumption progress.

Conclusion

Do not forget that the Nationwide Accounts information is three months outdated – a rear-vision view – of what has handed and to make use of it to foretell future traits will not be easy.

The info tells us that after the preliminary rebound from the lockdowns, progress continued to be average within the March-quarter.

Households are actually saving much less relative to their disposable earnings in an effort to keep up consumption progress within the face of rising rates of interest and short-term inflationary pressures.

I anticipate progress to say no additional and we can be left with rising unemployment and declining family wealth because of the RBA’s poor judgement.

That’s sufficient for at the moment!

(c) Copyright 2023 William Mitchell. All Rights Reserved.

[ad_2]